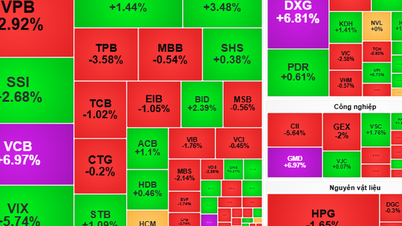

Pillar stocks lead, cash flow spreads widely

The acceleration was led by pillar stocks such as banks, securities, and real estate. VIC contributed nearly 11.5 points to the VN-Index, along with VPB, TCB, HPG, MBB, VHM... At the end of the week, cash flow shifted to mid- and small-cap stocks, notably in the steel, retail, chemical, and oil and gas industries.

On the contrary, some codes such asFPT , SJS, PNJ, FRT recorded less positive developments but had insignificant impact on the index.

The notable negative point is the net selling pressure from foreign investors, with a total value of nearly VND 12,900 billion - mainly from divestment transactions at VIC (approximately VND 12,500 billion). In addition, FPT, SSI, VHM, CTG are also under strong selling pressure. On the contrary, HPG, VPB, MWG, STG, NVL and TPB are among the group of net foreign buyers.

The market is in the stage of absorbing profit-taking pressure at the peak. Demand remains strong in key stocks, but cash flows tend to rotate between sectors. The tug-of-war is expected to continue early this week, before the uptrend is consolidated if cash flows spread and supply pressure cools down.

Technically, VN-Index could head towards the 1,600 - 1,640 point range if it maintains its momentum and cash flow operates effectively. However, risks of volatility and divergence still need to be noted.

The recommended strategy is to maintain flexible trading, prioritize short-term positions, and limit chasing when the market increases sharply. Investors can take advantage of the correction to restructure their portfolios, while closely monitoring reactions at the support zone of 1,550 - 1,570 points to manage risks.

Textile Industry: Opportunities in Challenges

The textile and garment industry is a key industry in Vietnam, contributing greatly to export turnover and creating jobs for millions of workers, especially in rural areas. However, this industry is sensitive to economic fluctuations and trade policies of major markets such as the US and EU.

In the period of 2022 - 2024, the textile and garment industry will be under a lot of pressure when the global economy weakens, inflation is high, and monetary policy is tightened, causing demand for garments to decrease. Orders from key export markets will decrease, while the heavy dependence on the US market (accounting for nearly 40% of export turnover) will increase risks.

Currently, the US is considering imposing a 20% tariff on some countries that are direct competitors of Vietnam, opening up great opportunities for domestic enterprises to attract shifting orders. The low preferential tax rate helps the industry improve its position in the global supply chain.

To take advantage of the opportunity, the textile and garment industry is promoting the localization of raw materials, developing specialized industrial zones, investing in green technology, and meeting international standards. At the same time, perfecting the value chain from fiber - weaving - dyeing - garment helps reduce import dependence, increase added value and sustainable competitiveness.

Source: https://phunuvietnam.vn/vn-index-thiet-lap-dinh-moi-ky-vong-dong-tien-tiep-tuc-lan-toa-20250811091005421.htm

![[Photo] General Secretary To Lam attends the opening ceremony of the National Achievements Exhibition](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/8/28/d371751d37634474bb3d91c6f701be7f)

![[Photo] Politburo works with the Standing Committee of Cao Bang Provincial Party Committee and Hue City Party Committee](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/8/28/fee8a847b1ff45188749eb0299c512b2)

![[Photo] National Assembly Chairman Tran Thanh Man holds talks with New Zealand Parliament Chairman](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/8/28/c90fcbe09a1d4a028b7623ae366b741d)

Comment (0)