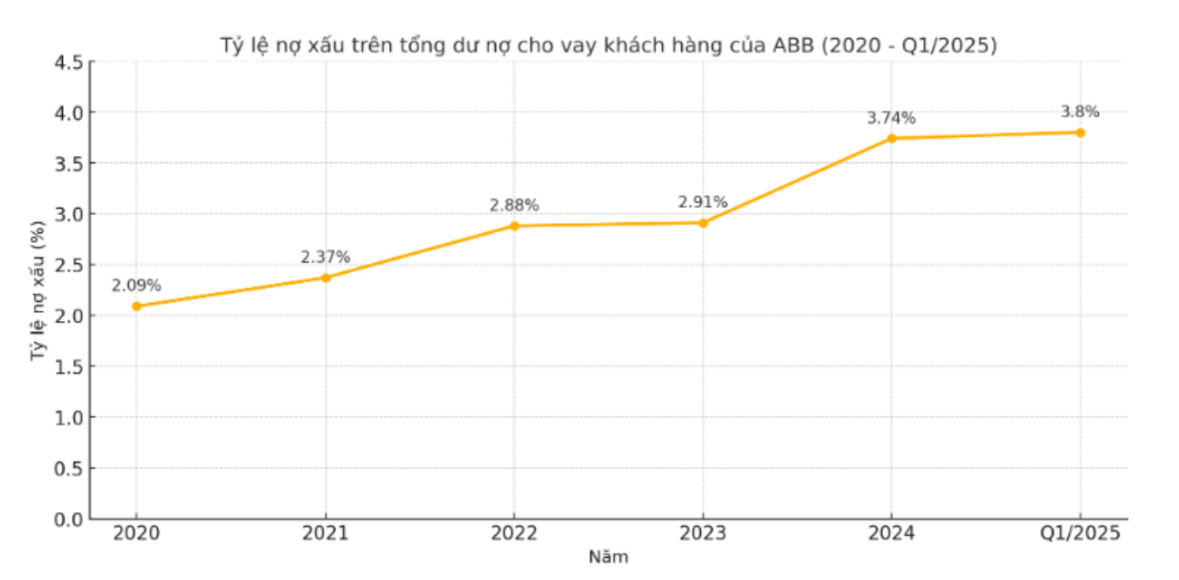

In the period 2020 - 2024, the bad debt ratio (total debt of groups 3, 4, 5) to the total outstanding loans to customers of ABBank increased steadily every year. In 2020, this ratio was 2.09%, increased to 2.37% in 2021, continued to 2.88% in 2022 and 2.91% in 2023. By 2024, the bad debt ratio had jumped to 3.74%, recording the highest level in this period.

The increase in bad debt comes not only from the proportion, but also from the structural shift to higher risk groups. In 2020, ABB's group 5 debt stopped at VND 622 billion, but by 2021 it had increased to VND 864 billion, then to VND 1,404 billion in 2022. By 2023, although it had leveled off at VND 1,035 billion, in 2024, group 5 debt suddenly increased sharply to more than VND 2,107 billion - nearly double that of the previous year and accounting for a large proportion of total bad debt. This is also the highest level that ABBBank has recorded in at least the past 10 years.

It is worth noting that while group 3 and 4 debt tends to fluctuate slightly, group 5 debt is increasingly expanding, showing that the ability to recover capital is becoming increasingly fragile. This raises a big question mark about the effectiveness of credit risk management at ABB, especially in the context of the whole industry tightening governance standards and increasing provisioning.

Entering the first quarter of 2025, the bad trend continues. According to the latest statistics, the total bad debt on the balance sheet at ABBBank has increased to VND 3,729 billion, of which group 5 debt continues to increase sharply to VND 2,278 billion - accounting for more than 61% of total bad debt.

Meanwhile, group 3 and 4 debt decreased slightly to VND613 billion and VND838 billion, respectively. The ratio of bad debt to total outstanding customer loans increased to 3.8%, significantly higher than the State Bank's control threshold of 3%.

At the 2025 Annual General Meeting of Shareholders, Chairman Dao Manh Khang affirmed that he would bring the bad debt ratio below 3%, even aiming for a target of 2% this year. However, with it exceeding 3% in the first quarter, this goal is increasingly distant.

At the same time, this development also shows that the banks' current solutions to handle bad debt are not really effective, requiring more drastic changes in the following quarters if they do not want to lose the trust of shareholders and the market.

Source: https://baodaknong.vn/ty-le-no-xau-tai-abbank-leo-thang-vuot-nguong-kiem-soat-nhom-5-cham-moc-cao-nhat-thap-ky-256489.html

![[Photo] The 9th Party Congress of the National Political Publishing House Truth](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/6/24/ade0561f18954dd1a6a491bdadfa84f1)

![[Photo] General Secretary To Lam meets with the Group of Young National Assembly Deputies](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/6/24/618b5c3b8c92431686f2217f61dbf4f6)

![[Photo] Close-up of modernized Thu Thiem, connecting new life with District 1](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/6/24/d360fb27c6924b0087bf4f288c24b2f2)

Comment (0)